The Dubai Golden Visa is a 10-year renewable UAE residency permit issued by the General Directorate of Residency and Foreigners Affairs — Dubai (GDRFA), the emirate-level authority that processes residency applications for Dubai-based investors. While the programme operates under the federal UAE Golden Visa framework, Dubai applications are administered through GDRFA and the Dubai Land Department rather than the federal ICP system used in other emirates — a distinction that shapes the application portal, documentation requirements, and processing timeline, though not the permit or its benefits.

Recent changes to GDRFA processing practice have reshaped how property investors access the programme. The qualification threshold for mortgaged properties has shifted from paid-up equity to DLD-certified total property value — meaning a AED 2 million property financed with a non-resident mortgage now qualifies where it previously did not. Separately, GDRFA and the Dubai Land Department have integrated property-linked residency services into a unified digital platform, reducing the co-ordination burden for applicants and improving processing timelines.

This Dubai Golden Visa guide covers the full GDRFA application process — qualification conditions for ready, off-plan, and mortgaged properties; the step-by-step submission sequence via the unified platform; documents required; and the approach for investors who want to co-ordinate property acquisition, mortgage approval, and GDRFA filing as a single transaction. The mechanics of the federal programme across all qualification categories and emirates are covered in the UAE Golden Visa.

Dubai Golden Visa: Property Qualification at a Glance

| Property Route | Qualification Basis | Key Condition |

|---|---|---|

| Ready property (outright purchase) | AED 2M DLD-registered value | Title deed must reflect registered value at or above threshold |

| Mortgaged ready property | AED 2M DLD-registered value | Outstanding mortgage balance not assessed; total DLD value applies |

| Off-plan property | AED 2M paid to developer | Oqood registration required; DLD total-value test does not apply until handover |

| Joint ownership | AED 2M per applicant | Individual registered interest at DLD must meet the threshold independently |

What Changed — New Rules Every Property Investor Needs to Know

Mortgaged Properties Now Qualify on DLD-Certified Value

Under the previous framework, qualifying for the Dubai Golden Visa through property investment required the investor to have paid-up equity of AED 2 million against the property. A property purchased at AED 3 million with AED 1.5 million paid toward the mortgage did not qualify; the investor needed to continue paying down the loan or hold a fully unencumbered property above the threshold. In practice, this excluded the large majority of mortgage-financed acquisitions — UAE lenders typically offer non-resident buyers 60–65% LTV in practice, which on a AED 2 million property means an equity position of AED 700,000 to 800,000 at acquisition, well below the former threshold.

Recent administrative guidance and current processing practice indicate that the paid-up equity condition no longer applies to mortgaged properties. Qualification is assessed against the DLD-certified total registered value of the property. A property purchased at AED 2.5 million with a typical NRI mortgage structure — for example at 60% LTV, AED 1 million in equity and AED 1.5 million financed — qualifies provided the DLD registration confirms total value at or above AED 2 million. The outstanding mortgage balance is not a disqualifying factor. Investors who were previously unable to qualify on properties above the AED 2 million DLD-certified value due to the equity condition may now be eligible to apply under current processing criteria.

The entry point for a mortgage-financed qualifying investment is a AED 2 million property at typical NRI LTV terms. Total equity required at acquisition — approximately 35–40% of the purchase price, 4% DLD registration fee, and approximately 2% in transaction costs — comes to approximately AED 820,000 to 920,000. That equity outlay generates both a qualifying investment and a 10-year renewable UAE residency permit, with the property’s income return running alongside throughout the hold period.

GDRFA-DLD Unified Platform — Consolidated Application Process

In April 2026, GDRFA and the Dubai Land Department signed a memorandum of understanding consolidating property-linked residency services into a single digital platform. The previous process involved three separate interactions: DLD title deed registration, an independent GDRFA application submission, and a DLD property verification step that GDRFA required before issuing the residency permit. Manual reconciliation between DLD and GDRFA records could introduce delays when documentation required verification across both authority systems.

The unified platform integrates DLD property data directly into the GDRFA application portal. For DLD-registered properties, GDRFA can verify ownership, registration value, and title deed status from the DLD database at submission — removing the need for a separate DLD verification step and the investor’s need to co-ordinate documentation between two authorities. Applications with complete documentation are often processed within several business days, although timelines vary depending on verification requirements and application volumes. The platform is accessible at gdrfad.gov.ae.

Qualification — Property Routes and Eligibility Conditions

The AED 2 Million Threshold — What the Number Means in Practice

The AED 2 million threshold is assessed against the DLD-certified registered value of the property, not the price agreed in the sale and purchase agreement or the price paid to the seller. DLD registers property value as part of the title deed issuance process, and this registered figure is what GDRFA uses to confirm qualification. In established demand corridors — Business Bay, Dubai Marina, Dubai Hills Estate, JVC, Al Furjan — DLD registered values track transaction prices closely. In segments with thinner comparable transaction data or newly opened supply areas, a modest spread between transaction price and DLD valuation can arise. Investors targeting the AED 2 million threshold precisely should confirm DLD valuation expectations with their conveyancing team before committing to a purchase price at the boundary.

Eligible properties must be in freehold designated zones — areas where foreign nationals hold full title deed ownership rights without a corporate intermediary. Freehold designated zones include Business Bay, Downtown Dubai, Dubai Marina, Palm Jumeirah, Dubai Hills Estate, Jumeirah Bay Island, JVC, Al Furjan, DIFC, and additional master-planned communities designated by decree. Properties in leasehold zones or outside freehold-designated areas do not qualify for the property route regardless of value.

Ready Properties — DLD Title Deed Route

Ready properties — units where construction is complete and a DLD title deed has been issued — are the most straightforward qualification route. The investor acquires the property, DLD registers the title deed at the transaction or assessed value, and the GDRFA application is filed via the unified platform immediately following registration. Under current GDRFA processing criteria, outstanding mortgage balance is not assessed — DLD-certified total value is the sole property-related criterion. The property must be registered in the individual applicant’s own name, or in a sole-ownership structure where the applicant’s individual DLD-registered interest is at or above AED 2 million.

Off-Plan Properties — RERA Oqood Route

Off-plan properties — units registered with the Real Estate Regulatory Agency before construction completion — are eligible provided the cumulative amount paid to the developer reaches AED 2 million. RERA issues an interim registration certificate (Oqood) in place of a title deed for off-plan purchases. GDRFA accepts the Oqood as proof of ownership for Golden Visa applications on this route. Current processing criteria apply the DLD-total-value test to ready mortgaged properties; off-plan qualification continues to use the paid-amount test, as DLD does not issue a full title deed with a certified value until handover.

For investors acquiring off-plan on a developer payment plan, the Golden Visa application can be filed once cumulative paid instalments reach AED 2 million — which on a AED 3 million unit with a 30:70 plan occurs at or around the first construction milestone payment. Investors targeting the Golden Visa from an off-plan acquisition should confirm from the developer that the Oqood reflects the accurate paid-amount figure, as GDRFA relies on the RERA-registered amount at the time of application.

Mortgaged Properties: Qualification Under Current Processing Criteria

The current qualification test for mortgaged ready properties: DLD-certified total registered value at or above AED 2 million. Qualification is assessed on DLD-certified registered value; the outstanding mortgage balance is not a disqualifying factor. For investors considering whether an existing mortgaged property now qualifies — or structuring a new acquisition — the key figure is the DLD-registered value on the title deed, not the loan outstanding or the original purchase price.

Sole Ownership — How Joint Acquisitions Affect Eligibility

Golden Visa qualification through property requires the AED 2 million to be registered in the individual applicant’s name at DLD. Joint ownership is assessed on each co-owner’s individual registered interest. A AED 3 million property registered equally between two owners records AED 1.5 million per individual at DLD — neither qualifies independently on that property. Investors in a joint acquisition where one or both parties want individual Golden Visa qualification should register the property with ownership shares that give each qualifying applicant at least AED 2 million in registered value, or acquire separate qualifying units.

The GDRFA Application — Step by Step

Step 1 — DLD Property Registration

For ready properties, DLD registration is completed at a DLD Trustee Office or via DLD’s Smart Services platform following transfer of funds from buyer to seller. The DLD registration fee is 4% of the transaction value plus AED 580 for title deed issuance. For mortgage-financed acquisitions, the bank’s security interest is registered on the title deed as an encumbrance note; the title deed is issued in the buyer’s name regardless of the encumbrance, and GDRFA draws this title deed from the DLD database to verify ownership and value. Trustee Office processing typically completes within one business day of fund transfer confirmation.

For off-plan properties, Oqood registration is managed by the developer through RERA following booking fee payment and execution of the sale and purchase agreement. RERA issues the Oqood certificate within 5–10 business days of receipt from the developer. The investor should confirm that the Oqood has been issued and that the paid-amount figure is correctly recorded before filing the GDRFA application — errors in the Oqood require developer-side correction which can delay the visa filing.

Step 2: Filing via gdrfad.gov.ae

The GDRFA application is filed through the GDRFA digital services portal at gdrfad.gov.ae under the Investor Residency / Golden Visa section. The investor creates or logs into their GDRFA account, then initiates the property-route Golden Visa application. Under the unified platform, DLD-registered property data is available to GDRFA directly — for properties registered under the integrated system, ownership and value verification is drawn from DLD without the investor uploading title deed documents separately. The application fee is payable at submission through the portal; the current fee schedule should be confirmed at gdrfad.gov.ae at the time of filing, as GDRFA fees are subject to revision.

Step 3 — Document Package

The standard document set for a property-route Dubai Golden Visa application via GDRFA: passport copy with minimum six months validity; a valid UAE entry permit or existing residency visa if the application is filed from within the UAE; title deed or Oqood for the qualifying property (drawn from DLD for registered properties under the unified system); Emirates ID application form; medical fitness certificate from a GDRFA-approved Dubai health centre; valid UAE health insurance; and recent passport photographs meeting GDRFA specifications. For mortgaged properties, the mortgage agreement is not required as a submission document — eligibility is confirmed on DLD-certified registered value accessed directly by GDRFA from the DLD system.

Step 4 — Processing, Residency Permit, and Emirates ID

Applications with complete documentation are often processed within several business days, although timelines vary depending on verification requirements and application volumes. GDRFA issues the residency permit — a visa label for in-country applicants, or an electronic entry permit for overseas applicants allowing re-entry for residency stamping and biometrics. Emirates ID is issued by ICP (the federal identity authority) following biometric capture at an ICP service centre. For Golden Visa holders, Emirates ID is issued with 10-year validity matching the residency permit term. The Emirates ID is the primary identification document for UAE banking, healthcare, school enrollment, and government services — biometric appointments should be booked promptly following permit issuance. A full comparison of qualification routes and processing authorities by emirate is set out in the UAE residency by property investment guide.

Mortgaged Property and the Dubai Golden Visa — An Integrated Approach

The Mortgage Approval Challenge for Non-Standard Income

The revised qualification framework has opened the Dubai Golden Visa to mortgage-financed acquisitions — but UAE mortgage approval for non-residents with non-standard income remains the primary bottleneck in the property-to-residency chain. UAE mortgage lenders apply CBU-mandated stress testing at current rates plus 200 basis points, require income documentation demonstrating repayment capacity over the full mortgage term, and typically require that income be presented in a form compatible with UAE underwriting assessment: salaried payslips, audited company accounts, or documentation that maps income streams to a recognisable lender template.

Investors whose income comes from business profits, carried interest, multi-jurisdiction rental portfolios, or dividend distributions frequently encounter difficulty through retail banking channels — not because their income is insufficient for the mortgage, but because the documentation does not conform to standard underwriting templates. A declined application creates a record that can affect subsequent applications with other lenders. The correct sequence is lender pre-selection matched to the investor’s income type and documentation structure, before any formal application is submitted.

Lender Selection and the Pre-Application Sequence

UAE mortgage lenders vary significantly in their appetite for different income types. Some apply rigid documentation templates that effectively exclude self-employed applicants, investors with multi-currency income, or those whose earnings are held in holding company structures. Others — including specialist non-resident lenders — assess income more holistically and have established frameworks for complex income files, particularly for NRI investors whose Indian income documentation requires preparation for UAE lender assessment. Identifying the right lender before submitting any application is not a procedural detail — it determines whether the mortgage clears at all.

Co-ordinating Acquisition, Mortgage, and GDRFA Filing

Helis operates across property acquisition, mortgage advisory, and GDRFA processing in a single engagement — which means property selection, lender identification, and Golden Visa filing are managed as co-ordinated decisions rather than handoffs to separate specialists. Property is selected with both yield profile and DLD valuation probability at the target threshold in view; the lender is chosen based on specific appetite for the client’s income structure; and the GDRFA application is filed immediately following DLD title deed registration rather than waiting for a separate advisory engagement to activate.

For investors restructuring a home-market-concentrated portfolio and wanting to combine the yield decision, leverage decision, and residency instrument in one transaction, the relevant planning context is set out in the NRI investment strategy guide.

The full mortgage advisory framework — lender selection for non-resident and NRI investors, income documentation structure, and the pre-application sequence — is set out in the UAE mortgage for property investors guide.

What the Dubai Golden Visa Delivers

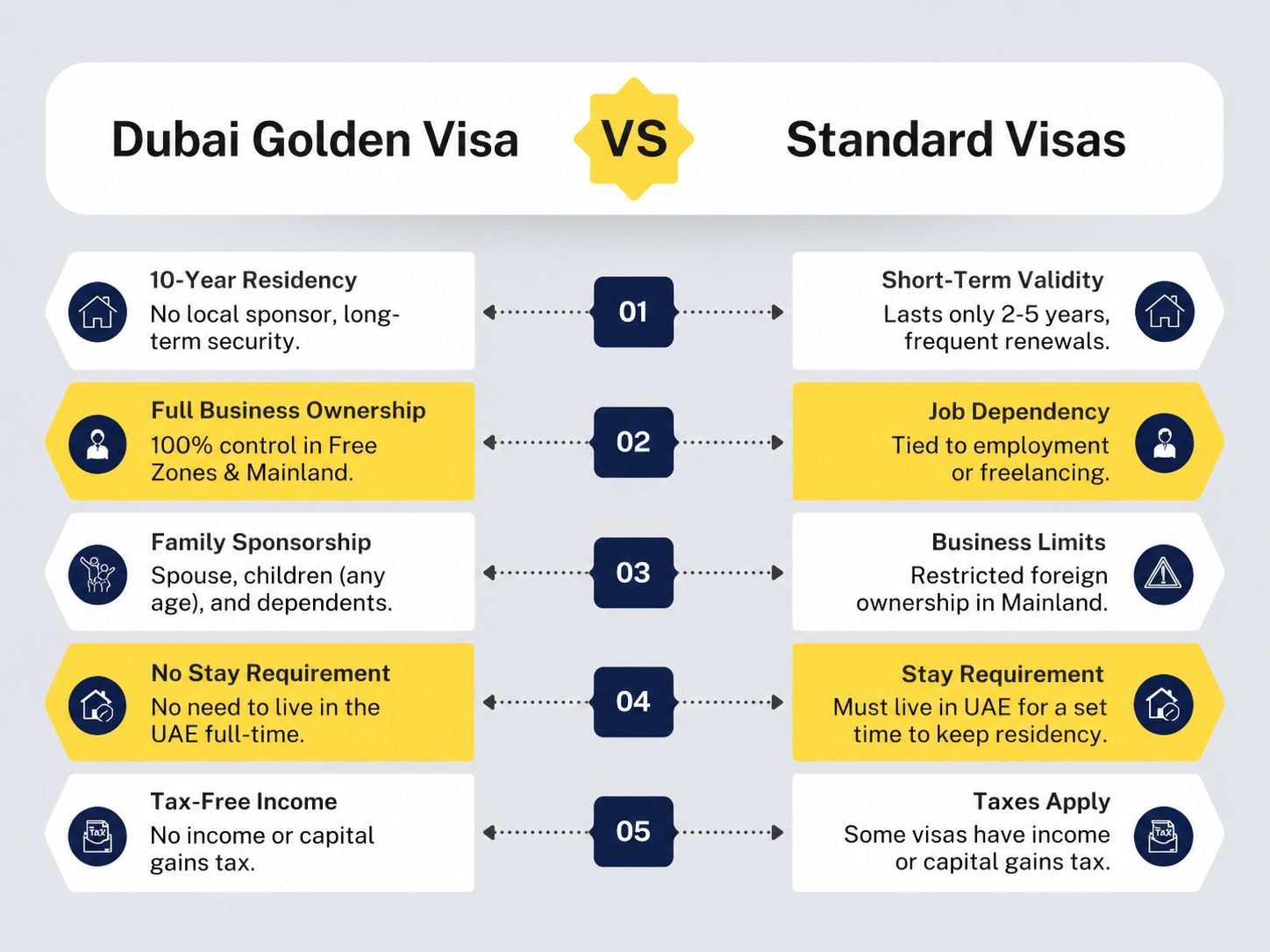

10-Year Renewable Residency with No Minimum Stay

The Dubai Golden Visa provides a 10-year renewable UAE residency permit. Unlike the standard UAE resident visa — which lapses if the holder is absent for six consecutive months — the Golden Visa carries no mandatory minimum stay requirement. The holder maintains legal UAE residency for the full 10-year term, subject to continued compliance with Golden Visa requirements. At renewal, the qualifying property must remain registered in the holder’s name at DLD with value at or above AED 2 million.

For investors who want UAE as a base of operations without relocating full-time — using Dubai for business travel, property management, banking, and family access while maintaining primary residence elsewhere — the Golden Visa creates a legal UAE presence that functions independently of employment, employer sponsorship, or periodic renewal cycles.

Family Sponsorship, Banking, and Day-to-Day Benefits

The Golden Visa holder can sponsor immediate family members — spouse and children — for UAE residency under the family sponsorship route, without dependence on employer sponsorship or the salary thresholds that apply to standard sponsor-based family visas. Domestic staff can be sponsored under standard UAE labour contracts. UAE banking relationships — more readily established with a UAE residency permit than a visit visa — remain active during periods of overseas absence without the residency-maintenance requirements that apply to standard visa holders.

For investors allocating UAE real estate as part of a broader portfolio repositioning, the residency instrument adds UAE school access, healthcare, and an established banking presence in a zero-income-tax environment — arising from the same capital deployed in the qualifying property, not a separate transaction in a separate jurisdiction. How this allocation fits within a portfolio repositioning is covered in the portfolio repositioning framework and the wealth planning guide.

UAE Residency and Tax Planning Sequencing

UAE residency establishes a legal presence in a jurisdiction with no personal income tax on employment income, business income, rental receipts, or capital gains from residential property disposal for individual investors in freehold zones. For investors simultaneously managing a home-market tax restructure — UK taxpayers working through the statutory residence test, Indian HNW investors managing FEMA and LRS compliance, European investors navigating exit tax frameworks — UAE residency status is a planning variable, not merely a travel convenience.

The ordering of residency establishment relative to home-market asset disposals and capital gains crystallisation is a material financial consideration; the correct sequence differs by home jurisdiction. This interaction — and how it fits within a co-ordinated wealth restructure — is addressed in the wealth planning guide.

Why Dubai Investors Apply Through GDRFA

GDRFA vs ICP — Two Parallel Systems for the Same Programme

The UAE Golden Visa is a federal programme — the same legal framework, qualification thresholds, permit term, and benefits apply across all seven emirates. The administrative distinction is in the authority that processes each application: GDRFA-Dubai (gdrfad.gov.ae) processes applications for Dubai-based properties and investors residing in Dubai; the federal ICP (icp.gov.ae) processes applications from Abu Dhabi, Sharjah, Ras Al Khaimah, Fujairah, and the northern emirates. The residency permit issued is identical — 10-year renewable, no minimum stay, full family sponsorship rights — but the application portal, document verification process, and processing timeline differ between systems.

For property-route investors, the determining factor is where the qualifying property is registered. A property with a DLD (Dubai) title deed uses the GDRFA route. A property registered with the Abu Dhabi Department of Municipalities and Transport or a comparable authority in another emirate uses the ICP route. Most investors targeting the Golden Visa through property investment are acquiring in Dubai — the freehold zone supply, mid-market yield profile, and the unified GDRFA-DLD platform make it the most direct path to property-linked UAE residency.

Property Selection and the Dubai Advantage

Dubai’s property market offers the broadest freehold zone designation of any UAE emirate, giving foreign nationals the largest pool of qualifying properties. Mid-market corridors — JVC, Business Bay, Dubai Hills Estate, Al Furjan — produce gross yields of 7–8.5% on properties in the AED 2–4 million range relevant to Golden Visa-qualifying investors, in a zero-income-tax environment where those net yields are retained in full. The full property selection framework — corridor analysis, DLD valuation expectations, off-plan vs ready, and leverage structuring — is set out in the Dubai real estate investment guide.

Dubai Golden Visa: Frequently Asked Questions

Can I get a Dubai Golden Visa with a mortgage?

Yes. Current GDRFA processing practice assesses eligibility against the DLD-certified total registered value of the property, not the paid-up equity. A mortgaged property with a DLD-registered value at or above AED 2 million qualifies regardless of the outstanding loan balance. This applies to ready properties; off-plan properties continue to use the paid-amount test under Oqood.

What is the minimum property value for the Dubai Golden Visa?

The threshold is AED 2 million, assessed against the DLD-certified registered value for ready properties, or the amount paid to the developer and registered via Oqood for off-plan. Properties registered jointly between two buyers are assessed individually: each applicant’s registered interest must reach AED 2 million independently.

Can I combine multiple properties to reach AED 2 million?

No. Current GDRFA processing practice assesses qualification on the value of the individual qualifying property. A portfolio consisting of multiple properties each below AED 2 million does not aggregate to meet the threshold. Investors relying on multiple assets should obtain confirmation from GDRFA before proceeding.

Does off-plan property qualify for the Dubai Golden Visa?

Yes, provided at least AED 2 million has been paid to the developer and the payment is registered under the Oqood system via RERA. DLD does not issue a full title deed for off-plan property until handover, so the paid-amount test under Oqood is the operative route. Once the property is handed over and a DLD title deed is issued, the qualification basis shifts to DLD-certified total value.

How long does GDRFA processing take for the Dubai Golden Visa?

Applications with complete documentation are often processed within several business days, although timelines vary depending on verification requirements and application volumes. The integrated GDRFA-DLD platform allows GDRFA to verify property data directly with DLD for properties registered under the unified system, which can reduce document burden and co-ordination time for applicants.

Do I need to live in Dubai to keep my Golden Visa?

No. The Dubai Golden Visa carries no mandatory minimum stay requirement. Unlike the standard UAE resident visa, which lapses if the holder is absent for six consecutive months, the Golden Visa allows the holder to maintain UAE residency for the full 10-year term without a minimum days-in-country obligation. At renewal, the qualifying property must remain registered at DLD with a certified value at or above AED 2 million.

Can I sponsor my family on my Dubai Golden Visa?

Yes. The Golden Visa holder can sponsor a spouse, children and other eligible dependants in accordance with current UAE Golden Visa sponsorship regulations. Eligibility criteria should be verified at the time of application as sponsorship rules may change. The primary holder does not need to be physically present in the UAE when processing dependant sponsorships through GDRFA.

What is the difference between GDRFA and ICP for Golden Visa applications?

GDRFA (General Directorate of Residency and Foreigners Affairs, Dubai) administers Golden Visa applications for Dubai-based properties and investors. ICP (Federal Authority for Identity, Citizenship, Customs and Port Security) handles the same programme for other emirates and certain professional-route applicants. Both issue the same 10-year federal Golden Visa permit. Dubai-based property investors apply through GDRFA via gdrfad.gov.ae; ICP applicants use the ICP Smart Services platform. Documentation requirements are broadly similar, but the administering authority determines the application portal, collection point, and primary contact for processing queries.

Does the Dubai Golden Visa affect my tax residency?

UAE residency is one factor some investors reference when establishing UAE tax residency, relevant where a home jurisdiction taxes on the basis of residency. The UAE itself imposes no income tax or capital gains tax. However, obtaining a UAE residency permit alone does not automatically change tax residency status under most home-country rules: additional tests based on days spent, centre of vital interests, or other criteria typically apply. Investors using the Golden Visa as part of a tax planning structure should obtain jurisdiction-specific legal advice before changing their residency status.

Investors who want to compare the property route against other Golden Visa qualification categories, or compare the Dubai programme against UAE-wide options, should review the UAE Golden Visa overview alongside the dedicated golden visa property investment rules guide. Helis co-ordinates property acquisition, mortgage structuring, and GDRFA processing in a single engagement — for investors whose Golden Visa application is part of a broader wealth restructure, the engagement starts with a property and financing structure optimised for both the investment return and the qualification conditions. For a detailed breakdown of qualifying zones, yield benchmarks and purchase timing, see our guide to Dubai Golden Visa property.