NRI investment strategy has shifted fundamentally over the past three years as Indian investors reassess where global capital should be structured, what jurisdictions offer the combination of yield, legal protection, and residency optionality that India’s domestic market cannot, and how the regulatory environment governing outward remittances interacts with long-term wealth planning. The UAE has emerged as the dominant destination for this reallocation — not because of proximity or cultural familiarity alone, but because the financial and legal case is structurally stronger than any comparable jurisdiction.

This NRI investment strategy guide covers the four pillars of a UAE-anchored allocation: real estate as the yield and appreciation engine, mortgage structuring for non-resident buyers, the Golden Visa as the residency layer, and the legal and tax framework that determines how much of the return the investor actually keeps. Each layer is interdependent — the decisions made in one affect the options available in the others, and the sequencing matters as much as the individual choices.

Why UAE Has Become the Core NRI Investment Destination

The Structural Shift Away from Western Markets

NRI investors have historically distributed capital across UK property, US equities, and Indian domestic assets — a three-jurisdiction structure that made sense when UK buy-to-let yields were competitive, US equities were in a structural bull market, and Indian equity markets were less mature. Each of those conditions has changed materially. In many UK buy-to-let structures, net yields after financing and taxation have compressed materially in recent years — often to 2.5–3.5% depending on ownership structure, tax bracket, and mortgage interest relief restrictions. US equities are priced at extended valuations with currency exposure for a rupee-based investor. Indian equity markets have matured and are now accessible domestically without the complexity of overseas investment structures.

The UAE offers something none of these markets can match: a zero-tax environment on rental income and capital gains at the UAE federal level for individual investors, a USD-pegged currency (AED at 3.67, held since 1997), freehold property ownership for foreign nationals in designated zones, and a residency programme — the Golden Visa — that converts a capital deployment into a ten-year legal status. For an NRI investor evaluating where to concentrate cross-border allocation, the UAE’s structural advantages are not marginal. They are decisive.

FEMA, LRS, and the Regulatory Framework for Outward Remittance

Indian nationals remitting capital overseas operate under the Liberalised Remittance Scheme (LRS), which permits remittances of up to USD 250,000 per financial year per individual for permitted purposes including property purchase, investment, and maintenance of relatives abroad. For HNW investors deploying amounts above the annual LRS limit, the transaction is structured across multiple financial years or through corporate vehicles — a legal and well-established approach that requires proper documentation at the point of remittance.

Resident Indians purchasing property abroad must comply with FEMA regulations governing outward capital transfers. Non-resident Indians — those holding NRI status under the Foreign Exchange Management Act — have broader flexibility in structuring overseas investments, as their foreign-sourced income is not subject to the same LRS framework. The distinction between resident Indian, NRI, and Person of Indian Origin (PIO) status is relevant to how the overseas investment is structured and what repatriation rights apply at exit. This is territory where the investment decision and the legal structuring should be reviewed together, not sequentially. Investors should obtain India-qualified tax and FEMA advice before structuring cross-border remittances or overseas property acquisitions.

Real Estate — The Core Allocation Anchor

Yield, Appreciation, and the Net Return Advantage

Dubai mid-market residential — units in the AED 900,000 to AED 2.5 million range across JVC, Business Bay, Dubai Hills, and Al Furjan — produces gross rental yields of 7–8.5% and net yields of 6.5–7.5% after service charges and management fees. For an NRI investor with rupee-denominated income, the AED’s long-standing peg to the USD gives the income stream relative dollar stability — converting what would otherwise be an emerging market property play into a hard-currency income position. The yield differential against UK property (often 2.5–3.5% net after tax depending on structure) or Indian residential property (2–3% gross) is substantial and structural, not cyclical.

Capital appreciation in established Dubai corridors averaged 15–20% per annum across 2022–2024, driven by a structural shift in end-user demand rather than speculative inflow. Some investors underwrite mid-market corridors on the assumption of moderate long-term appreciation — often in the 5–8% range — based on supply absorption data and population growth trajectories, though past performance does not guarantee future returns. Combined with net yield of 6.5–7.5%, total annual return in the 12–15% range is achievable in well-selected corridors, with full capital gain retained on exit at zero CGT. The Dubai real estate investment guide covers the market entry framework in detail.

Segment Selection — What NRI Investors Should Target

Not all Dubai real estate is equally well-suited to an NRI investment profile. Luxury units above AED 5 million in Palm Jumeirah and DIFC offer prestige positioning and trophy asset appeal, but yield 3–5% gross — too compressed to justify the allocation on a return basis for most NRI investors whose primary objective is yield and appreciation rather than trophy positioning. Mid-market corridors — JVC, Business Bay, Dubai Hills Estate — produce the yield outcomes that make the investment case, with a broader end-user buyer pool at exit that provides stronger resale liquidity.

The AED 2 million threshold is a meaningful marker in segment selection for NRI investors because it aligns with the Golden Visa qualifying level. An investor targeting a single property allocation should evaluate whether sizing to AED 2 million or above — to access the residency benefit alongside the financial return — changes the risk-adjusted case. For many NRI investors, the residency optionality the Golden Visa provides is worth the incremental allocation above a lower entry point.

Mortgage Structuring for NRI Buyers

LTV, Rates, and the Non-Resident Ceiling

Non-resident buyers in the UAE — including NRI investors who do not hold UAE residency — are limited to 50% LTV on residential property purchases, regardless of income level or asset base. This is a regulatory ceiling set by the UAE Central Bank, not a lender policy, and it applies uniformly. On a AED 2 million purchase, the maximum mortgage is AED 1 million; the buyer must provide AED 1 million in equity plus the 4% Dubai Land Department fee and approximately 2% agency commission. Total cash required at acquisition: approximately AED 1.16 million on a AED 2 million purchase with 50% LTV financing.

Current non-resident mortgage rates are pricing at 5.5–6.0% all-in on EIBOR-linked variable products. At AED 1 million financed over 25 years at 5.75%, the monthly repayment is approximately AED 6,300 — serviceable against monthly rental income of approximately AED 11,000–12,500 on a AED 2 million mid-market unit. The debt service coverage is positive from day one in a well-selected corridor, which means the leveraged position is cash-flow positive even at current non-resident rates.

Complex Income Files and the Specialist Mortgage Case

NRI investors frequently present income profiles that UAE bank underwriting systems handle poorly: Indian-sourced self-employment income, equity compensation from technology companies, dividend income from family businesses, or multi-jurisdiction income that does not fit neatly into the salary-slip documentation standard that UAE banks use as their primary underwriting input. Standard bank channels decline structurally sound applications at the initial assessment stage because the documentation does not match the checklist — not because the borrower cannot service the debt.

Specialist mortgage advisory for complex NRI files involves selecting lenders whose underwriting methodology is appropriate for the income type, constructing the documentation to present the income in terms the lender’s credit committee can approve, and advocating through the credit process where a standard bank relationship manager does not. Complex but financially strong NRI applications can often be approved through the UAE mortgage process when structured through lenders familiar with non-standard income profiles — the cost of specialist advice is frequently recovered in the first year through a mortgage that a standard channel would have declined.

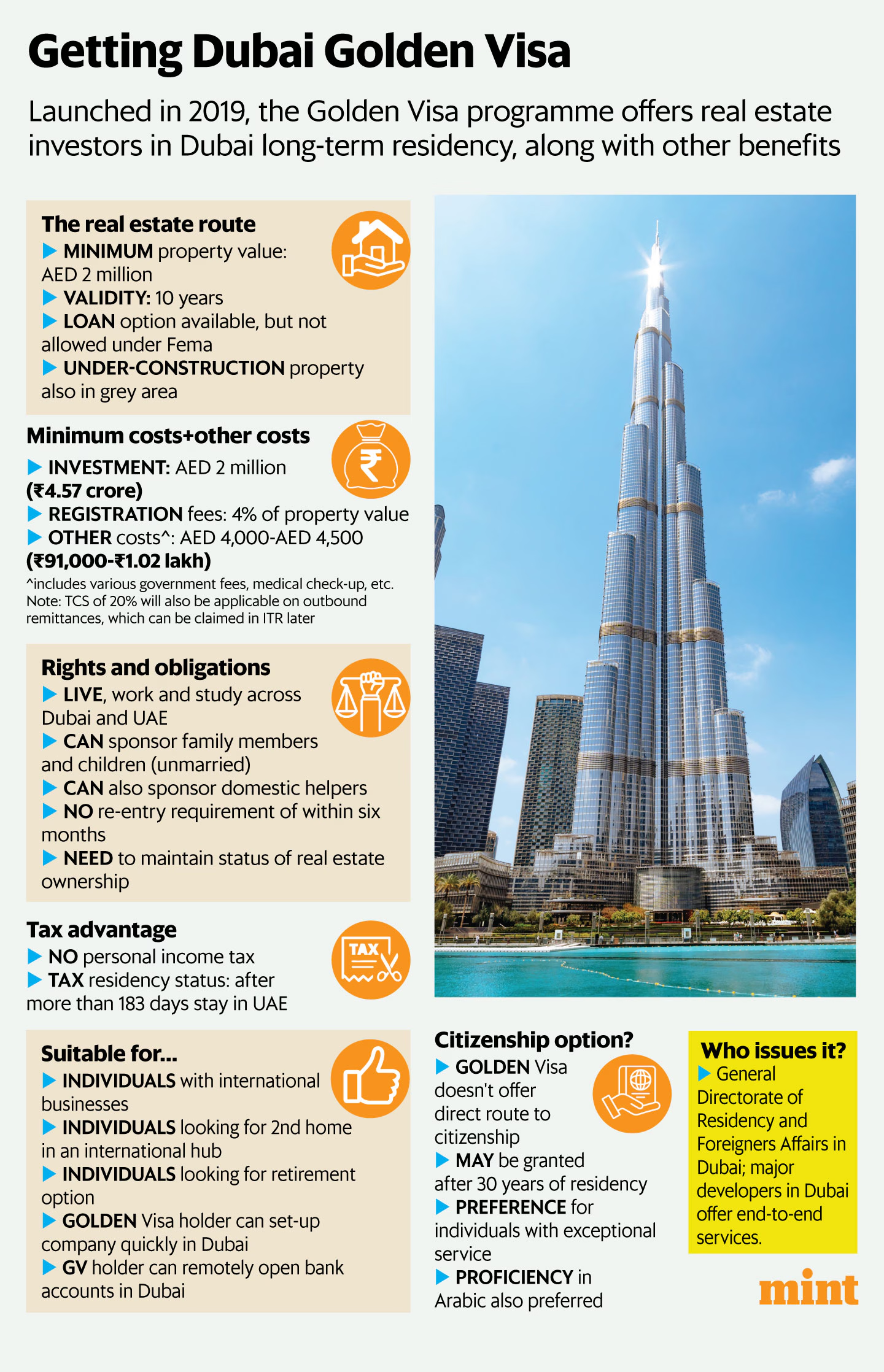

The Golden Visa — Residency as Part of the NRI Strategy

Qualification, Timeline, and What the Visa Actually Provides

UAE property purchases at AED 2 million or above — in the buyer’s own name, not through a company — qualify for the Golden Visa: a 10-year renewable UAE residency permit with no minimum annual stay requirement, full family sponsorship rights for spouse, children subject to prevailing UAE dependency and sponsorship rules, and domestic staff, and access to UAE banking, healthcare, and school enrollment without employer sponsorship. For NRI investors, the Golden Visa provides a UAE operational base that complements India-based life without requiring relocation — the investor can spend time in the UAE when needed for business or personal reasons, without visa runs or sponsorship dependency.

The Golden Visa processing timeline from property registration to visa issuance runs approximately four to six weeks for standard applications. The process involves title deed registration with the Dubai Land Department, a property valuation confirming the AED 2 million threshold, and the residency application processed through the General Directorate of Residency and Foreigners Affairs. For families, each member’s visa is processed separately — the sponsor (property owner) is processed first, then dependants. The UAE Golden Visa page covers eligibility, documentation, and the full process in detail.

Golden Visa Within a Broader NRI Mobility Structure

For NRI investors who are evaluating second citizenship or permanent residency in parallel with the UAE allocation, the Golden Visa operates as the operational base layer of a broader mobility structure — UAE for business and tax residence, a Caribbean or European citizenship programme for programme-independent travel document and permanent legal status that does not depend on property ownership maintenance. The distinction between residency by investment and citizenship by investment is material for NRI investors who want both the UAE’s practical advantages and the security of a second passport that cannot be lost if the property is sold.

Executing the NRI Strategy Through a Coordinated Advisory

An NRI investment strategy anchored in UAE real estate involves decisions across property acquisition, mortgage structuring, Golden Visa processing, and legal entity considerations — all of which are interdependent and time-sensitive. The property selection determines the Golden Visa eligibility; the financing structure determines the cash required at acquisition; the visa timeline interacts with the mortgage drawdown schedule. Executing through separate advisers in each domain creates coordination gaps that add cost and delay and sometimes result in structuring errors that are difficult to unwind after execution.

Helis operates across real estate, mortgage, and citizenship advisory for HNW investors — designed to coordinate the cross-domain decisions that a UAE-anchored NRI strategy requires. The advisory engagement covers the full execution process from market entry and lender selection through to title deed and visa issuance, managed as a single integrated workflow rather than sequential handoffs between specialists. For NRI investors evaluating a UAE allocation, the starting point is the real estate advisory engagement, which scopes the full execution plan before any capital is committed.